Average EU white sugar prices have continued to climb through 2023/24, rising higher again from last year’s unprecedented levels.

The rise in average prices for sugar sold this campaign has not been as stark in sterling as it has been in euro terms, but nonetheless the average value of sugar being sold by beet processors and refiners remains the highest recorded since EU price reporting began in 2006.

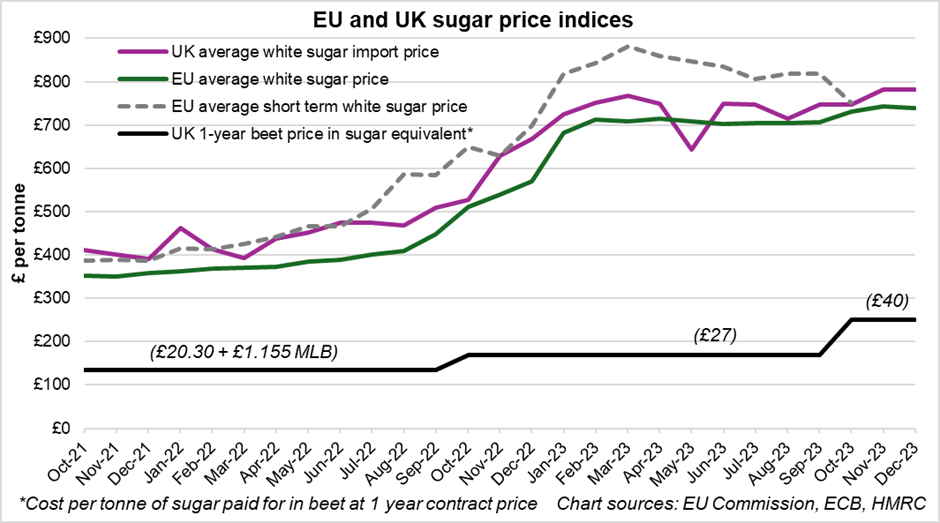

There is no equivalent price transparency in the UK sugar market, but the UK sugar market operates as part of the wider European sugar market. UK prices generally track at a premium to the EU price reflecting the deficit between homegrown sugar production and demand, which is reflected in the price paid by UK buyers of imported white sugar.

This is the only publicly available information on the price paid for sugar in the UK covering both contract and spot transactions.

The price of sugar remains high and gradually rising in large part because the vast majority of sugar sales are made at contract prices agreed in the months leading up to campaign, while spot sales account for a tiny minority.

EU Commission data for the last campaign shows that spot prices rose well above the pre-agreed contract price levels, likely driven by the frost issues seen in the UK and elsewhere in 2022/23, leading to a very tight sugar supply across the European market.

By contrast, spot prices in 2023/24 are reported (for example, by S&P Global) to be lower than the overall average sugar sales price, although official EU Commission short term price reporting is not yet available past October 2023.

The consensus is that after contract prices were agreed for 2023/24, yields across Europe have proven to be better than average (if not exceptional), beet area proved higher than was thought in the summer, and the impact of c.450Kt of Ukrainian sugar entering the European market in 2023 duty free is being felt.

Margin between beet cost and sugar prices exceptionally high

Nonetheless, the margin between the cost of each tonne of sugar purchased in beet and the price of sugar continues to sit well above the level two years ago.

As shown, even with beet at £40/t in 2023/24 (equalling a farmgate value of sugar of £250/t), this leaves a margin of over £500/t, before adding on co-product incomes, to cover processing, extraction and transport costs (using the price of white sugar imports as a proxy for the UK sugar market).

This contrasts with a margin around £300/t, on the same basis, in 2021/22.

This will feed directly into the processor’s profitability, dependent on whether processing, extraction and transport costs have risen by this scale in the past two years.

There is a widespread expectation that contracted sugar prices will not reach the same levels for the 2024/25 campaign, though would still be very high by historical standards.

This is underpinned by a strong world market but a reduced European premium (based on expectations of a greater beet planted area in both the UK and EU as reported previously).

In general, the price at which sugar is contracted in Europe tends to reflect 1) the world price at the time the deal is made and 2) a premium driven by the volume of imports the market expects to need to balance.

Futures Linked Contract trading open

Trading opened on the 2024 Futures Linked Contract on Friday 9 February, following creation of the formula by Czarnikow. Please note the final formula has been calculated at Oct-24 no.11 raw sugar futures - £148.67/t.

Read our futures-linked sugar beet contract explainer to find out more.

A trader’s view

NFU Sugar Board appointee and sugar trader Paul Harper shares his thoughts on the current market situation.

NFU Sugar Board appointee Paul Harper

Paul has spent his entire career in commodities and has been in sugar since 1976. He joined C Czarnikow in 1973 working in their London, New York and Singapore offices. Paul has a huge amount of consultancy experience, having consulted for a hedge fund, major bank and a large trade house in sugar during that time.

Over the past few weeks the market has done very little.

Rain in South Brazil has interrupted some shipments but not by enough to cause major concern for the time being.

Elsewhere in the world, upcoming crops are being watched closely, largely to do with weather concerns.

There appears little appetite from producers to hedge at current levels, especially with the discounts showing in the more forward months, and whilst the speculative element have reduced their long positions to close to neutral, sugar’s fundamentals remain constructive going forward so they are unlikely to switch to short positions any time soon.

The current South Brazil crop is coming to a close and it will be interesting to see how much sugar is produced in 2024/25.

Expectations are for a similar number as last year and the market definitely requires it to be so to avoid the deficit getting any larger.

With the world market almost entirely dependent on one country for supply, any changes in production numbers to the downside will almost certainly cause a spike in prices.

With the futures linked formula having been fixed, beet prices have fallen below the £40/t level on the market for the time being, however, the downside from current levels is likely to be minimal.

The WABCG view: Speculators are no longer betting on a fall...

Taken from the World Association of Beet and Cane Growers’ Flashmarket newsletter on 7 February, by Timothé Masson, Executive Secretary of WABCG and economist for the French beet growers association, CGB.

You will remember that sugar fell last month, abandoned by speculators. In January, the trend was the opposite: raw sugar rose by 10% over the month and speculators, who used to expect the market to fall, have returned to a balanced position; it seems that they can’t figure out whether the market is going up or down.

Such a balanced position is rare in the sugar market. What could cause speculators to buy or sell?

Clearly, the fact that production in Brazil or India is better than expected is now “into the market”, i.e. taken into account by operators in their price forecasts. So we have to look further ahead to anticipate new developments, and that’s where it gets tricky.

Some dare to make forecasts (Czarnikow, for example, expects a world surplus of 1.6Mt for the current season, before a deficit for the following season), but many are waiting for April and the start of the new Brazilian season: will it be as exceptional as the previous one, with ethanol finally showing signs of recovery? What will be the impact of El Niño in the coming months – including in the next Indian campaign in October?

But instead of trying to anticipate the future, let’s take a look at this equilibrium in speculators’ positions: it is not without interest. On the contrary: despite this equilibrium, the raw sugar market remains above 23c/lb. The last time it was at this level was in 2016 and speculators had a lot to do with it: they were net buyers of 12Mt of sugar!

A high market with no speculation: we could be tempted to conclude that the current value of the market seems quite robust...