Campaign progress in the UK has been affected by the wettest autumn, and more widely the wettest second half of the year, since 2000 in East Anglia.

This has impacted beet harvesting and supply into factories, but has not been unique to the UK. Similar weather impacts have affected countries across the European beet belt.

In addition, this is likely to be factor in the average sugar content in beet for the campaign so far remaining below 16% as covered in much more detail in January’s BBRO BeetCast. If this remains the case for the remainder of the campaign, 2023/24 would be the first time since 1976/77 that the average UK sugar contents has dropped below 16% – even in recent frost and VY (Virus Yellows) affected years, the campaign average remained above 16%.

The impact of the wet weather is arguably more acute for beet supply elsewhere in Europe than in the UK.

The typically long campaigns in the UK, with beet processing generally expected to continue into March in any case, mean that there are still at least two months of opportunity for the wettest, heaviest fields to become suitable for lifting.

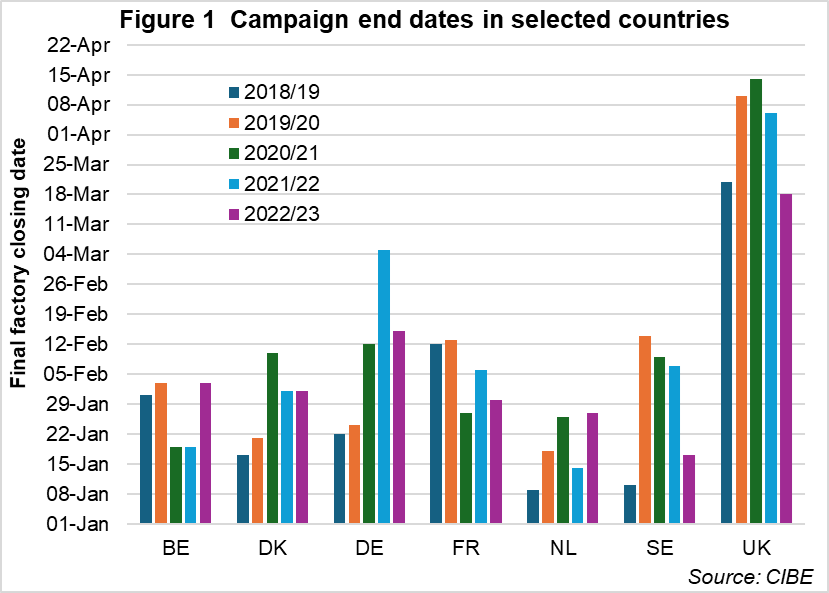

However, in countries facing similarly wet weather like northern France, Belgium and the Netherlands, it is unusual for campaigns to continue beyond early February at the very latest (see figure 1). Therefore, in these countries there are concerns among the growers that not all fields will become suitable for lifting before factories need to close, with NFU Sugar hearing that potentially around 5% of the beet area could be at risk in the latter two cases.

European beet area to increase in 2024

After a rebound in European beet area for 2023, most expectations are that beet area will increase by another few percent once again in 2024. One driver of this is that, compared to 12-18 months ago, sugar, and hence anticipated beet, prices have remained strong in comparison to prices of other crops.

Subject to eventual stock carry over from 2023/24 into 2024/25, future EU trade policy towards Ukrainian sugar imports, and of course European beet yields in 2024 which are impossible to forecast at this point, all else being equal, this potential increase in planted area is anticipated to reduce the premium of European and UK sugar prices over world markets in 2024/25 from the exceptionally high levels it reached in 2023.

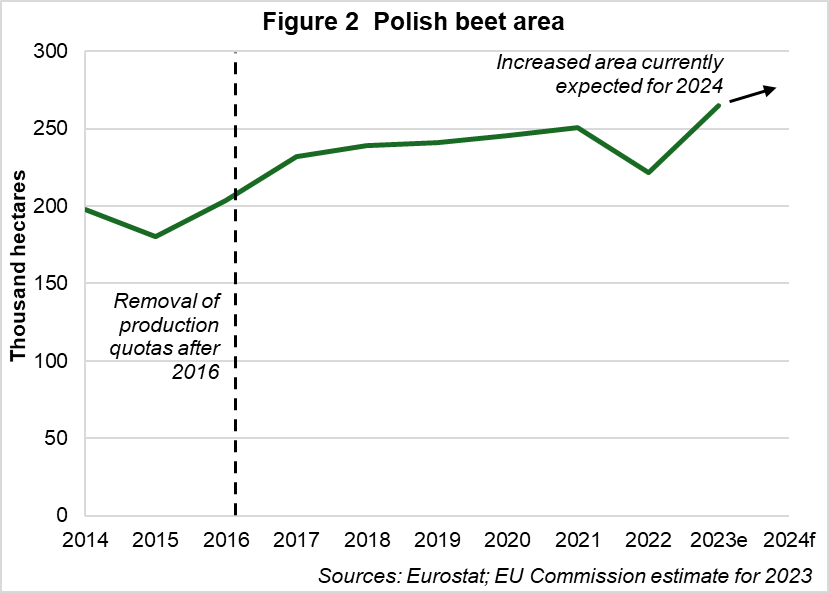

In 2023, a major driver of the European area increase was a substantial increase in Polish beet area, and in 2024 this is expected one of the countries where planted area rises again. As shown in figure 2, this is one of the few countries in Europe where beet area has risen consistently since the end of quotas in times of both low and high prices, in contrast to France for example which saw a large increase then a subsequent drop in beet area post-quota.

Despite this consistent expansion, the Polish sugar industry remains a beneficiary of coupled support. Traditionally, the western European beet belt has been the main sugar surplus region driving European sugar markets, but this trend could continue to increase the sensitivity of the European market to weather and dynamics in Eastern Europe.

A trader’s view

NFU Sugar Board appointee and sugar trader Paul Harper shares his thoughts on the current market situation.

NFU Sugar Board appointee Paul Harper

Paul has spent his entire career in commodities and has been in sugar since 1976. He joined C Czarnikow in 1973 working in their London, New York and Singapore offices. Paul has a huge amount of consultancy experience, having consulted for a hedge fund, major bank and a large trade house in sugar during that time.

Since our last review the market has had a dramatic move to the downside, falling more than $175/t in the raw sugar market and almost $170/t in white sugar before the year end. Since the beginning of 2024 prices have stabilised and begun to move higher gaining around $40/t in both markets at the time of writing.

This downside move, which was a surprise to many, was initiated by an increased expectation of the South Brazil crop by around 800Kt, which was then followed by a notification from India that some ethanol production would be switched back to sugar.

Both fundamentally bearish items provoked selling from the speculative element in the market, which fed upon itself as the market began to move lower. From being over 200,000 lots (10Mt) long in the raw and white sugar markets combined, their positions declined to almost nil towards the bottom of the move.

Interestingly, as far as India is concerned, the export ban has not been lifted and the extra sugar that will be produced is therefore unlikely to be exported, especially at the lower levels, and will be added to the low stock levels held within the country for local consumption.

Looking at the 2024/25 supply/demand figures, even with the increase in the South Brazil 23/24 crop, there is still an expected deficit. The market therefore is unlikely to fall below the levels already seen in the short term.

Supply is still very reliant on South Brazil and any disruption from this region will likely bring a sharp reaction to the upside in prices.

The market may well have overstretched in price, both at the high and low end of the recent move. However, if the expected deficit going forward materialises, it is likely that higher prices will be seen as we go through the year.

The WABCG view: a sharp fall close to 2023

Taken from the World Association of Beet and Cane Growers’ Flashmarket newsletter on 5 January, by Timothé Masson, Executive Secretary of WABCG and economist for the French beet growers association, CGB.

If you have only one chart to look at today, it should be the one showing speculators’ positions. From being net buyers of more than 6Mt of sugar at the end of November, they ended 2023 as net sellers (0.1 Mt). What happened during this crazy month?

It started with a revision of the Brazilian forecast on 30 November: CONAB (Brazil’s national agricultural statistics agency) estimated production at 46.8Mt (instead of its first forecast of 46.0Mt).

Then, on 8 December, the Indian government announced that green juice (freshly pressed cane) could not be used for ethanol production: it would have to be kept for sugar production. Although the equivalent of 5Mt of sugar was expected not to be produced because of ethanol, the figure is now expected to be between 3.0 and 4.5Mt.

Finally, on 14 December S&P published a new forecast in which they expect a surplus of 4.4Mt. This explains the strong movement of speculators, even more so than at the end of December, as funds usually like to publish a balanced situation at the end of their financial year. Will it last? For many, the situation is exaggerated. Consumption is still the great unknown of the campaign, and Czarnikow expects a surplus of only 0.2Mt. Moreover, if sugar falls below 20-21c/lb, buyers would be happy to consolidate sugar stocks - at the lowest levels almost anywhere in the world. Finally, everyone seems to have forgotten that the main impact of El Niño on fundamentals will be felt in the coming months.

And indeed, after losing 20% in US dollars (even more in Mexican pesos or Thai baht), raw sugar slowly recovered. White sugar followed, with the white premium remaining very strong ($140/t), showing that demand for ready-to-use sugar remains strong in the short term.

This very volatile month for sugar was an exception: grain, oil and freight were much calmer.